LIBRARY

THAILAND 国・地域情報 会計・税務

【THAILAND】UPDATED: Announcement Regarding Salary Levels for Foreigners Working under the BOI Privileges

Overview

Updated, FAQ public announcement by BOI

On June 5, 2025 (date of promulgation), the Thailand Board of Investment (BOI) issued Notification No. 8/2568, outlining the appropriate employment ratio of Thai nationals working under approved incentives and various regulations concerning the employment of foreigners.

The following table shows the minimum monthly salary (average monthly income) stipulated for foreigners working under these regulations, with the effective dates as follows:

- For incentives approved before the date of promulgation: Applicable from the January 2026 salary.

- For incentives approved after the date of promulgation: Applicable from the October 2025 salary.

In practice, this will be checked when renewing work visas and work permits.

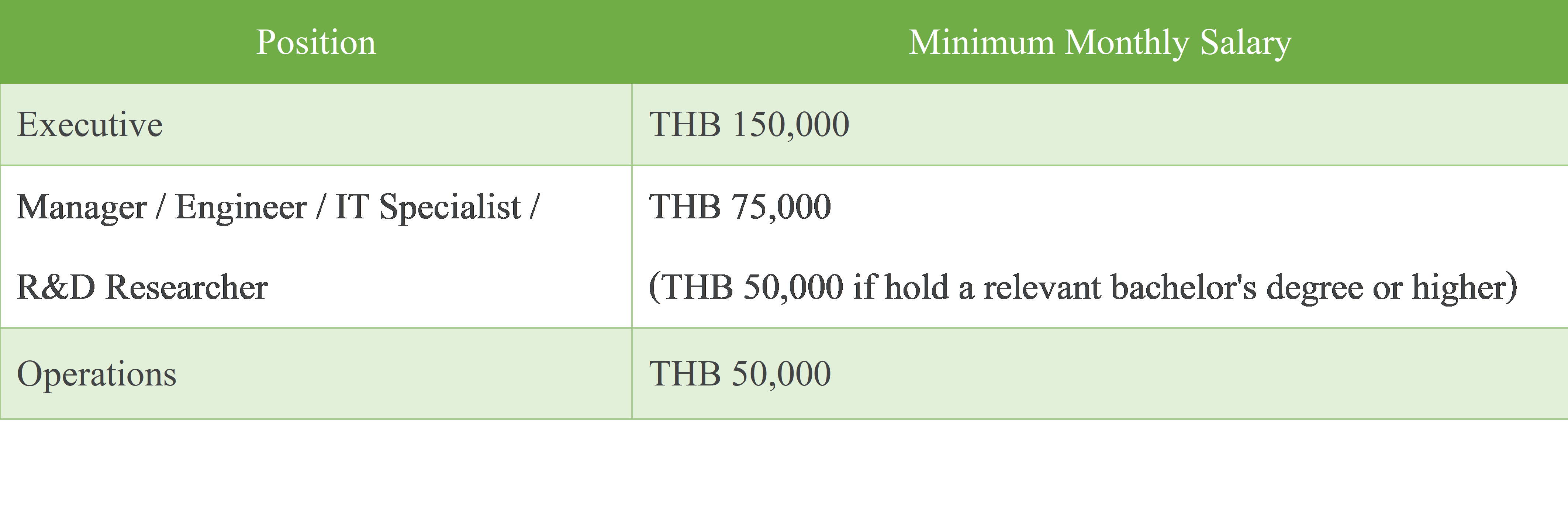

Minimum average monthly salary for foreigners: This was stipulated as follows for each position

Explanation:

In the previous explanation, we stated that the BOI’s intention was to assume that the Thai company would pay the full amount of the salary to the foreigner.

However, the FAQ clarified that overseas-paid salaries may be included in the minimum average monthly income to meet this minimum average monthly income requirement. However, a requirement has been added that at least 50% of the total salary must be paid by a Thai company under BOI benefits.

When renewing work visas or work permits, the BOI stipulates that for foreigners working in Thailand year-round, the annual salary income summary (PND1Kor) will be used to consider whether this minimum average monthly income requirement is met. For those working in Thailand for less than one year, the monthly withholding tax declaration (PND1) will be used. Therefore, in the former case, it is likely that the monthly salary amount will be checked by dividing the annual salary income by 12 months.

Recommendation:

Even if the monthly salary paid by a Thai company falls below the minimum average monthly income standard, if the company receives salaries from overseas, such as from a parent company, we recommend that the Thai company consider filing and paying taxes on such overseas salaries together with the Thai salary on a monthly withholding tax return (PND1), rather than filing them on an annual individual income tax return (PND91). This is because if the taxes are filed monthly, the overseas salary will be included in PND1Kor.

If you have any concerns, please do not hesitate to contact us.

Contact Us

please fill in this form.